You have finally crossed the finish line. After two or three years of grueling assignments, stressful exams, and balancing a part-time job, you have officially graduated from your Canadian college or university. Even better, your Post-Graduation Work Permit (PGWP) has just been approved in the mail. You are now ready to start your professional career and make real, full-time money.

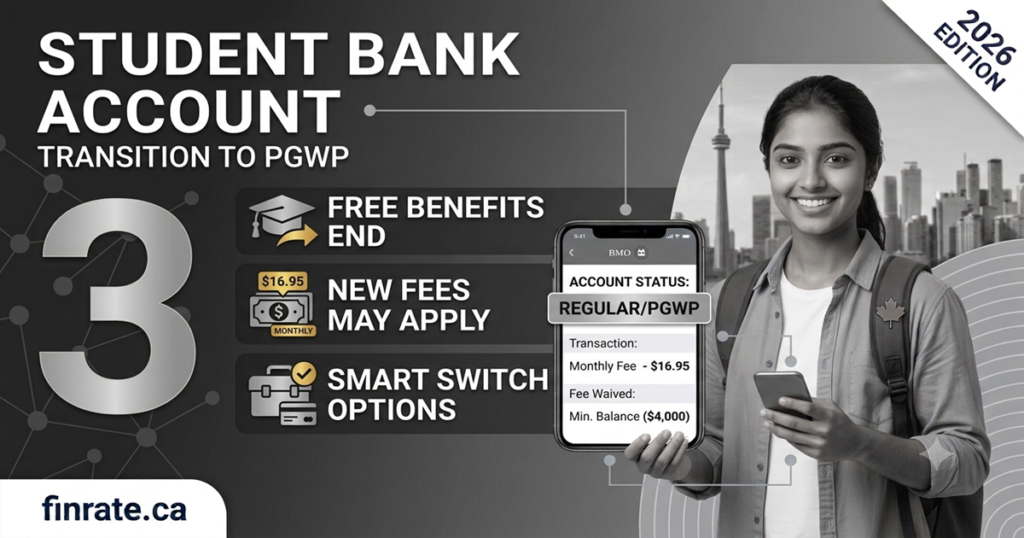

Everything feels perfect until you open your mobile banking app at the end of the month and notice a sudden, unexpected charge: “Monthly Account Fee – $16.95.” You call your bank, confused, and the customer service agent tells you that because you are no longer a full-time student, your free banking privileges have been permanently revoked.

Welcome to the PGWP Banking Trap.

For years, Canadian banks have offered international students completely free, premium chequing accounts. However, this is not out of the goodness of their hearts. It is a calculated strategy. They know that once you graduate and get a PGWP, you will likely be too busy or too lazy to switch banks, allowing them to quietly transition you into an expensive adult account.

In this complete 2026 guide, we will explain exactly how banks track your graduation date, what happens to your student credit cards, and the top three strategies you can use to avoid paying monthly banking fees forever.

How Does the Bank Know You Graduated?

When you first arrived in Canada and opened your bank account using your Study Permit, the bank representative asked you for your “Expected Graduation Date.”

This date was hardcoded into your banking profile. The bank’s internal computer system is programmed to track this specific month and year. When that date finally passes, the system automatically triggers a transition protocol.

Usually, the bank will send a polite, generic letter or email warning you that your “Student Advantage” period is ending. If you ignore this letter (which most students do, thinking it is just marketing spam), the bank will automatically convert your free student chequing account into a standard “Everyday Chequing Account.”

Suddenly, you are being charged anywhere from $11.95 to $16.95 every single month just to keep your money in the bank. Over a year, that is nearly $200 vanished into thin air!

Strategy 1: The “Minimum Balance” Waiver

If you love your current big bank (like Scotiabank, CIBC, RBC, or TD) and you do not want the hassle of changing your direct deposit information with your new employer, there is a very common way to waive the monthly fee.

Almost every major bank in Canada offers a Minimum Balance Waiver.

- How it works: If you maintain a specific minimum balance in your chequing account for the entire entire month (usually between $3,000 and $4,000), the bank will completely waive your monthly fee.

- The Catch: Your balance cannot drop below that required number for even a single day. If your rent comes out on the 1st of the month and your balance drops to $2,999, you will be charged the $16.95 fee for that month.

While this is a convenient option, it is not always financially smart. Leaving $4,000 sitting in a chequing account that earns zero interest means you are losing money to inflation. That $4,000 could be growing tax-free inside an investment account instead!

Strategy 2: Ask for the “New Graduate” or “Alumni” Offer

Do not accept the monthly fee without a fight. The Canadian banking sector is highly competitive, and banks desperately want to keep you as a customer now that you are a full-time worker.

Before your student account expires, walk into your local branch or call customer service and ask if they have a “Recent Graduate Program.” Many of the “Big Five” banks offer a one-year grace period for recent graduates. For example, they might offer you a premium chequing account completely free for another 12 months, or give you a heavy discount on the monthly fee to help you transition into the workforce.

Financial Tip: You can also leverage your profession. If your PGWP allows you to work as a registered nurse, engineer, or accountant, many banks offer heavily discounted “Professional Banking Packages” specifically tailored to your career path. Always ask the teller what specialized packages are available!

Strategy 3: Switch to an Online-Only Bank (The Best Choice)

If you are tired of playing games with minimum balances and temporary graduation offers, it is time to make the smartest financial move for your PGWP era: Switch to a digital bank.

In Canada, there are several “Online-Only” banks (sometimes called Challenger Banks). Because these banks do not have physical branches to pay rent on, and they do not have to pay thousands of tellers, their operating costs are extremely low. They pass these savings directly to you by offering 100% free chequing accounts with zero minimum balance requirements.

The two most popular digital banks for newcomers and PGWP holders are:

- Tangerine Bank: Owned by Scotiabank, this digital bank offers a completely free chequing account. Even better, because they are owned by Scotiabank, you can use any Scotiabank ATM across Canada for free to withdraw or deposit cash.

- Simplii Financial: Owned by CIBC, Simplii operates on the exact same model. You get unlimited free e-Transfers, zero monthly fees, and free access to all CIBC ATMs nationwide.

Switching your daily transactions to Tangerine or Simplii is the ultimate “set it and forget it” strategy to ensure you never pay a banking fee in Canada again.

What Happens to Your Student Credit Card?

While your chequing account will automatically change and start charging you fees, the rules for your credit card are very different.

If you have a student credit card (like a basic cash-back or rewards card with a $500 or $1,000 limit), the bank will not cancel it, nor will they suddenly start charging you an annual fee. That specific credit card product is yours to keep for as long as you want.

However, graduating and getting a full-time job on a PGWP means your income has significantly increased. This is the perfect time to optimize your credit.

- Ask for a Credit Limit Increase: Now that you have a real salary, you can easily call your bank and ask them to raise your credit limit from $1,000 to $3,000 or $5,000. This will dramatically lower your credit utilization ratio, which will boost your Canadian credit score.

- Do a “Product Transfer”: Do not cancel your student credit card, as closing your oldest credit account will hurt your credit score. Instead, ask the bank to do a “Product Transfer.” They can seamlessly upgrade your basic student card to a premium, high-reward adult credit card (like a World Elite Mastercard or Visa Infinite) while keeping your credit history completely intact.

Frequently Asked Questions (FAQs)

Can the bank freeze my account if my Study Permit expires?

Yes, they can. Under Canadian banking regulations, banks must ensure their clients have legal status in the country. If your Study Permit expires and you have not updated your profile with your new PGWP document, the bank may temporarily freeze your account for compliance reasons. Always bring your physical PGWP into the branch as soon as you receive it!

Can I keep my student account if I take a one-year break?

No. Banks verify your student status every single September. They do this by checking if you have an active enrollment record or by asking you to provide a current timetable. If you take a gap year, you cannot keep your free student banking privileges.

Is it hard to switch my direct deposit to a new online bank?

Not at all. If you decide to switch to a free digital bank like Tangerine, you simply download a digital “Void Cheque” from their mobile app and email it to your employer’s HR or payroll department. Your next paycheque will automatically route to your new free account.

Welcome to the Professional World

Graduating and securing your PGWP is an incredible achievement. Do not let the major Canadian banks sour the moment by draining your hard-earned money with unnecessary monthly fees.

By understanding how the system works, leveraging minimum balance waivers, or making the permanent switch to a free digital bank, you can keep 100% of your new salary exactly where it belongs: in your pocket.

(Now that your everyday banking is free and your income is growing, it is time to start investing! Read our complete guide on Can International Students Open a TFSA? to learn how to grow your money tax-free in Canada.)

1 thought on “What Happens to Your Free Student Bank Account When You Get a PGWP? (2026 Guide)”